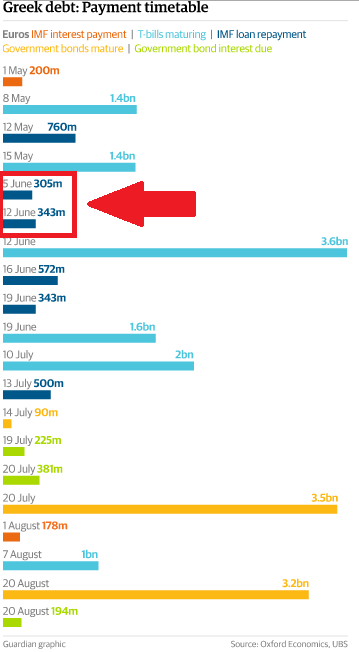

On May 15 Greece has to “roll over” €1.4B in debt, which means sell more debt to pay debt, or borrow money to pay money back. They can do that because the banks keep buying more T-Bills. What they can’t do is pay the IMF anymore. €305M on June 5. €343 a week later. There is no more money left in the IMF monopoly account at the IMF to pay the IMF back with. There’s nothing left.

A Greek default, or any government default for that matter, is heavily misunderstood. I’m not speaking in terms of chain reactions here or what it may cause, just essentially what it is.

If a private person defaults, say if I go bankrupt, that means anyone who I owe money to, loses that money that I would have paid them. That’s it. Not one person who did not loan me anything will suffer at all. People who have no financial connection to me couldn’t care less if I default since it has nothing to do with them.

It gets a bit more complicated if I own a business. If I go bankrupt, my business will be sold by force for lack of payment of my debts, someone else will get the business and do what he wants with it, and the cash I got for the sale will go to my creditors in order of liens. All the capital I control, whatever it is, goes to someone else, and the cash goes to my creditors. That’s what happens. No capital is destroyed, nothing changes physically, just ownership titles.

So, if a government goes bankrupt, what SHOULD happen by that example is they stop paying their debts, which are their bonds. Then, by the example of myself going bankrupt and my assets being liquidated and transferring title to some other owner, what should happen and what WOULD solve the entire garbage situation in Greece is for the entire government to liquidate ALL of its asset, everything it owns, and sell it ALL for cash, in this case Euros.

Entire Greek government departments should be sold to whoever wants them for however much is offered. If someone wants the Greek Bureau of Regulation Whatever and to employ all its pointless bureaucrats, then they can. But you know what the problem is here?

If I go bankrupt but I own a business, my business probably makes money, just not enough to cover my debts. It has employees etc. So somebody buys it, maybe lays off a few people, ships up the outfit and makes it profitable

But who the HELL wants a piece of crap bureaucracy? It makes no money, it only obstructs business!So bidding for it would go through the floor and be equivalent to whatever hard assets the Bureau has like computers and real estate and cars and whatever, and all the dumb bureaucrats would be laid off and that’s it.

The other problem is the government owns the roads, and for some reason everyone is brainwashed into thinking that roads cannot be privately owned because then 1,250,000 people would die on the roads globally every year. But wait, no, that’s how it is now.

So the government owns assets that people don’t believe can be sold, when of course they can and should.

But the worst part of government default is that the government owns the money itself, because money is a government monopoly. So when a government defaults, anyone who holds government money is in serious, serious trouble. They will lose everything. Holding government money is like being a government employee when your employer goes bankrupt. It is bad. That’s why people own gold and silver.

The unique problem with Greece, however, is that the government there does not own the money supply. And that’s why they can’t print the currency to death and need bailouts. Germany and Brussels and the ECB own the money supply.

If this default were honest, everything the Greek government owned or controlled would be liquidated and sold, including the Hellenic Parliament building itself and all the roads and all the military equipment, absolutely everything, with cash raised to pay the bonds. All the bureaucrats would be laid off to find something to do in the economy. All the regulation enforcers would be unemployed. The economy would be freed.

A true, honest government default would be an absolutely great thing for the private citizen, if not for the fact that the government, instead of honestly going bankrupt like any private person and starting over at zero, will immediately set itself up another monetary monopoly, force everyone to use it, and inflate it to death, stealing from everyone just to stay in business.

If Greece starts printing drachmas, they will hyperinflate very quickly. If I were a Greek, I would buy real assets and hide them under the Parthenon. That, or sell all paper assets short now.

When a private person or company goes bankrupt, assets are liquidated and sold to new owners. Employees are let go and must find new jobs. Some stay.

When a government goes bankrupt, they destroy everyone else’s money so they can pay back their debts through theft. Greece is just a tiny little thing, a tiny domino in a line of ever increasing bankrupt dominoes.

When the US goes bankrupt, now that will be a sight to see.

We’re headed for default in Greece. Varoufakis may have human guts, but he’s still clueless, still doesn’t understand that the Everlasting Gobstopper doesn’t actually exist. That the government cannot simply supply endless resources at a whim. Just doesn’t get it.

Tsipras of course doesn’t get it. So it’s funny I should be reading this headline on Ynet first, in Hebrew. The other headlines to the same story do not catch the punchline. But the Israeli headline does. For example, Reuters:

“Defiant Greek PM sets up EU clash with bailout rejection, austerity rollback”

Ah, but the Jews get it. They get that you can’t solve an insolvency problem by handing out free stuff. Ynet, on the same story:

ר”מ יוון מציג: חשמל ומזון חינם לעניים

Greek Prime Minister Lays Out Plan: Free Electricity and Food for the Poor

Yeah, that’ll do it. That should put you right back on the road to financial stability. Hand out more free crap. Suck on the Everlasting Gobstopper that is government money.

What’s happening here, from what I can see, is a crazy angry Prime Minister with extreme Greek pride is combining with a confused Finance Minister with the guts to push Europe to the brink and over, with neither realizing at all the meaning of their “solutions”.

We’re on our way to default. The eurozone is going down folks, in weeks to months. Brace yourselves.

BAM! Yanis Varoufakis was just confirmed as Greece’s new finance minister. I’ve been writing about Varoufakis since 2012. You can see all the posts I’ve written about him here.

First off, no he is not a libertarian. BUT he is genuine, he is not a politician (yet), and he’s got fire in his soul. That much I can tell. I’ve been fascinated with him for years because he has been the lone (and loan) voice of sense in the entire Greek mess. While he is not a libertarian and believes in government regulation, he does know and understand that the state is the entrepreneur’s biggest enemy. This much he said in a recent interview.

He’s articulate, speaks like a human being instead of in moronic soundbites and brainfarts that make you want to vomit, and his English is impeccable. And he doesn’t fake his conviction say, like Elizabeth Warren.

Oh, and he isn’t a fat disgusting lizard-looking slob of an embarrassment like his predecessor Evangelos Venizelos. (I only insult politicians for being physically repulsive.)

I mean really, which guy would you want to be a Finance Minister? This guy:

Evangelos Venizelos, Fat Lizard Man

Or this guy:

Yanis Varoufakis

No contest. He also understands how the current bailout setup is only bleeding private Greek citizens to the last drop.

What happens is this. A government spends too much money loaned to them by fractional reserve banks that are inherently unstable. The government then scares everyone into believing that if it defaults, the planet will explode. Therefore, private taxpayers are scared into giving up a bunch of money so the government can keep paying the banks their interest, which if they don’t get, could start a chain reaction of bankruptcies due to the inherent instability of fractional reserve banking. Meanwhile the private economy has no capital left to grow the economy because it’s all going to the government that keeps paying off the banks.

In the case of the Greek bailout, it is all of Europe’s taxpayers that has to finance the Greek government, so it’s much worse.

Varoufakis’s solution you can listen to here, which I wrote about almost 3 years ago. It’s a little nutty at the end where he wants to Europeanize the entire banking system which will have the effect of spreading out Greece’s government’s losses over the entire Eurozone. This will dilute the effect, but won’t solve the problem. It’ll just put it off for another decade or so until the entire continent’s governments collectively run up their debts even higher.

But in any case, it doesn’t matter. Varoufakis won’t get that far. He’ll insist on defaulting, which really is the only honest thing to do. Better say you can’t pay and go home than rob taxpayers even more just so you can keep paying interest payments a little longer while your debt keeps going up anyway. Am I sure it’s going up? Yes.

I’ll keep saying it, but once Greece defaults, there will be a crazy bond run on Italy. Italy will fall, and then the Eurozone will either split or collapse entirely.

But if anyone has the guts to push the default button and see what the hell happens, it’s Yanis. I’m totally psyched.