BAM! Yanis Varoufakis was just confirmed as Greece’s new finance minister. I’ve been writing about Varoufakis since 2012. You can see all the posts I’ve written about him here.

First off, no he is not a libertarian. BUT he is genuine, he is not a politician (yet), and he’s got fire in his soul. That much I can tell. I’ve been fascinated with him for years because he has been the lone (and loan) voice of sense in the entire Greek mess. While he is not a libertarian and believes in government regulation, he does know and understand that the state is the entrepreneur’s biggest enemy. This much he said in a recent interview.

He’s articulate, speaks like a human being instead of in moronic soundbites and brainfarts that make you want to vomit, and his English is impeccable. And he doesn’t fake his conviction say, like Elizabeth Warren.

Oh, and he isn’t a fat disgusting lizard-looking slob of an embarrassment like his predecessor Evangelos Venizelos. (I only insult politicians for being physically repulsive.)

I mean really, which guy would you want to be a Finance Minister? This guy:

Evangelos Venizelos, Fat Lizard Man

Or this guy:

Yanis Varoufakis

No contest. He also understands how the current bailout setup is only bleeding private Greek citizens to the last drop.

What happens is this. A government spends too much money loaned to them by fractional reserve banks that are inherently unstable. The government then scares everyone into believing that if it defaults, the planet will explode. Therefore, private taxpayers are scared into giving up a bunch of money so the government can keep paying the banks their interest, which if they don’t get, could start a chain reaction of bankruptcies due to the inherent instability of fractional reserve banking. Meanwhile the private economy has no capital left to grow the economy because it’s all going to the government that keeps paying off the banks.

In the case of the Greek bailout, it is all of Europe’s taxpayers that has to finance the Greek government, so it’s much worse.

Varoufakis’s solution you can listen to here, which I wrote about almost 3 years ago. It’s a little nutty at the end where he wants to Europeanize the entire banking system which will have the effect of spreading out Greece’s government’s losses over the entire Eurozone. This will dilute the effect, but won’t solve the problem. It’ll just put it off for another decade or so until the entire continent’s governments collectively run up their debts even higher.

But in any case, it doesn’t matter. Varoufakis won’t get that far. He’ll insist on defaulting, which really is the only honest thing to do. Better say you can’t pay and go home than rob taxpayers even more just so you can keep paying interest payments a little longer while your debt keeps going up anyway. Am I sure it’s going up? Yes.

I’ll keep saying it, but once Greece defaults, there will be a crazy bond run on Italy. Italy will fall, and then the Eurozone will either split or collapse entirely.

But if anyone has the guts to push the default button and see what the hell happens, it’s Yanis. I’m totally psyched.

There’s a Mises.org article circulating now about how the recent Greek elections could end up shattering the Eurozone. This really is uncharted territory because nothing like the Eurozone has existed before, with separate sovereign states sharing a fiat currency controlled by a central bank.

The article is titled “How Greek Default May Still Unravel the EU“. Despite a few strange contradictions between the beginning and the end of the article, what I found most interesting was this part:

Greece currently owes a little over 300 billion euros to various creditors. About 200 billion is owed to the Eurozone institutions, the European Financial Stability Facility (EFSF), and the European Stability Mechanism (ESM), that raised funds based on Eurozone guarantees…Spain, Italy, and France have guaranteed about 50 percent of this debt. A default would mean an important increase in the debt load of each of these countries. This would likely be the tipping point for Italy which has a current debt to GDP level of over 130 percent and several decades of essentially no growth. Italy is too big to bail out.

I did some cursory Googling of anything about Italy guaranteeing any portion of Greek debt. I couldn’t find anything, but I didn’t really put much effort into the research. There are no footnotes to the article, so I see no source for this, though that doesn’t mean it isn’t true.

Let’s assume it is though. Tsipras and Varoufakis together are a pretty formidable force for getting out of the current debt stranglehold. Varoufakis wants to default and hates politicians. Tsipras wants to maintain his fiery appeal and may just be crazy enough (in a good way) to listen to Varoufakis, who is probably the only honorable person in the entire Hellenic Parliament to have any grasp of economics at all.

If Tsipras can’t get a good deal enough to appease his voters – and nothing will appease them because their expectations are ridiculous – then Varoufakis will egg him on to default within the Euro. Now, whether this actually increases Italy’s debt burden due to guarantees through the ESM and EFSF seems rather unimportant, because if Greece defaults, I’m willing to bet that Italian bonds are going to plummet the next day with Italian interest rates skyrocketing. That will be enough to push Italy overboard.

If Greece defaults at 175% debt to GDP with bond investors losing everything, Italy is not far behind at 133%. Nobody is going to want Italian bonds in the event of a bona fide Greek default. If Italy goes down, then so do the rest of the PIIGS – leaving Portugal, Ireland, and Spain. What happens then is really up in the air. Nobody knows.

But yes, a Greek default will fundamentally alter the Eurozone if not destroy it.

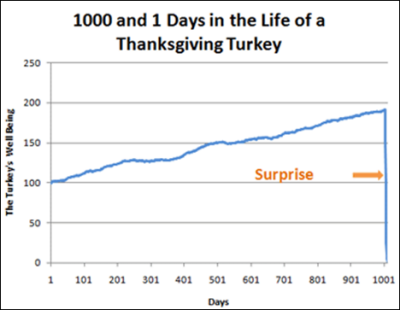

Nicholas Taleb’s book The Black Swan has this chart at the beginning explaining what the Black Swan is. It’s a chart of the life of a turkey up until the day before Thanksgiving. Here’s the chart.

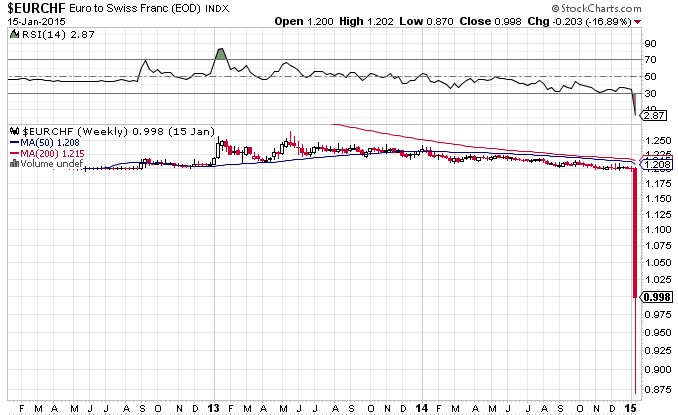

Here’s an eerily similar chart from January 15th of the Euro traded in Swiss Francs.

The point is, when central banks do something unexpected, the markets can flip in ways that will shock you.

The Swiss National Bank decided it was too expensive to keep a 1.20 Euro to Swiss Franc peg. In order to maintain that they had to buy a bunch of Euros and take them out of circulation with Swiss Francs they would print and put into circulation. Basically absorb the inflation that the European Central Bank was creating and stick it on its balance sheet.

By November 2014, the SNB had absorbed 475B Swiss Francs worth of foreign currency. At that point they decided it was too much. So all they did was say they were no longer buying Euros, and the Euro fell through the floor.

475 billion. That’s it.

Do you know how many US Dollars China has on its balance sheet, sopping up American inflation like a neverending sponge that just will not saturate? Almost $4 trillion. That is about 8.5x the amount of Euros the SNB had when it announced it was no longer buying Euros, and the Euro fell 30% in a day.

Can you IMAGINE what will happen to the US dollar when – not if, but when – China says it is no longer buying?

And keep in mind that the SNB never said it was selling any of its Euros. Just that it would stop buying them.

Now, here is the $4,000,000,000,000 question. Can you fathom what would happen to the US dollar, the US economy, treasury bonds, the Federal government, if and when China announces not only that it will no longer buy US dollars, but that it will actually sell them? Try to get something for its paper they’ve been stacking there for decades?

Here is the simple truth. Economic armageddon is in the hands of the People’s Bank of China. All it has to do is announce they are selling their dollars, and the game is over. That’s it. The only thing stopping them is that for some crazy reason, the Chinese think that it benefits them to import American inflation.

When they figure out that it only hurts them, they will simply stop doing it.

The Swiss National Bank already figured it out. It now looks like the Danes are next.

I love this guy, but I don’t understand him. He’s got some things so right, and others so wrong. Yanis Varoufakis was just interviewed on Bloomberg about what should be done in Greece. He’s a pleasure to listen to because unlike other smug econometrician academic weasels, you can tell Varoufakis is sincere and has some sort of moral drive. The problem is, he’s confused. He understands Greece is bankrupt. He doesn’t seem to understand that the politicians he is joining do not understand that that essentially means they can no longer spend money.

In his latest interview with Bloomberg, Varoufakis made some pretty frank comments. Among the most frank was his answer to the question “Do you know for sure if the bailout will be renegotiated, or if SYRIZA will make a U-turn?” meaning, will SYRIZA cave and just keep going with the bailout in order not to get kicked out of the Eurozone in a so-called Grexit.

His answer reminded me of what Ron Paul said to the question “Will the Federal Government default?”

“The government will default. It’s just a question of how, through outright default or inflation.”

Varoufakis answered this question the same way. The bailout will be renegotiated, simply because the current bailout makes no damn freaking sense. How can a bailout from debt put you more in debt? How is that even a bailout? That’s just doing CPR on a corpse. (My words, not his.)

Dealing with the issue of a Grexit, Varoufakis said that in “brushing off” a Grexit as containable, the sponsoring Eurozone countries were basically making up bullshit. They have no idea what the consequences will be, because nobody knows who holds how many bonds where, and what the systemic effects will be, whether other bond runs will ensue, it’s like trying to predict exact weather patterns 2 years in advance.

In short, there can be no Grexit without severe consequences for everyone, and those brushing it off have no idea what they’re talking about.

So much he gets. What he doesn’t get is that when Greece does default, which will absolutely happen in one form or another, his politician friends, the same nincompoops that have co-opted him as their voice of reason in SYRIZA, will want to ramp up the spending once again, because that’s all they know how to do.

He will be in the extremely uncomfortable position, likely as finance minister, of saying no. There is no money, there is nothing, stop trying to spend what doesn’t exist. If he can maintain his candor, he will end up resigning.

At the end of his interview with Bloomberg, he was asked what must be done. He said something very libertarian. Paraphrasing, entrepreneurs in Greece face one big enemy, and that is the State. The State does not let them put people back to work because it punishes them with taxes that make no sense. The economy is totally paralyzed by the State apparatus, and that is why the State is bankrupt.

In Rothbardian terms, the parasite overwhelmed the host, and now both have died.

Someone who can speak in such clear libertarian terms, I don’t know what he’s doing joining a radical left wing political movement expecting them to just sit back and relax as he recommends they shrink government. There’s going to be a big fight between him and Alexis Tzipras. They are on a collision course.

Once the bailout is renegotiated, Tzipras will want to spend more money on his projects. Varoufakis will tell him there is no money. Tzipras will then want to print Drachmas until they have no value, which will happen very quickly if he tries to print them.

There is nothing SYRIZA or New Democracy, or Pasok can do to get money. There just isn’t any. They will all come flying at a brick wall of bankruptcy, because there is no one left to steal from. It’s all gone. Only Varoufakis understands that. He won’t be able to explain it to the politicos. They don’t get it. They never will.

This makes absolutely no sense, which is why the Swiss Franc (CHF) just had the most insane trading day in its history. It was up by as much as 30% against the Euro this morning, and is now up something like 15%. Currencies don’t move that way unless something really strange is up.

This makes no sense because the Swiss National Bank (SNB), just a few months ago, came out hard against the Swiss Gold Initiative, saying it was crazy and dangerous precisely because it would cause the CHF to skyrocket. The purpose of the Gold Initiative was to muzzle the SNB at a 20% gold reserve so they couldn’t keep printing CHF in order to support the Euro. This robs purchasing power from Swiss consumers, and is basically stealing.

So now that they have basically said they will stop printing CHF to support the Euro, they seem a bit schizophrenic. They have basically just done exactly what the Swiss Gold Initiative was going to force them to do, so everyone is really confused.

Gold, by the way, is up about 2.5% on the news.

My guess is that the SNB is fearing a Eurozone collapse in the next few weeks/months when SYRIZA is elected in Greece and goes sour on the bailout, forcing a Grexit. Just a Grexit does not pose existential danger to the Eurozone, but if it causes a bond run on Portugal or Italy, the whole pair of dirty underwear that is the Eurozone is going to unravel at the seems and Europe will be exposed in all its monetary nakedness.

The SNB, back in November when it railed against the Swiss Gold Initiative, was assuming the Euro would float back up eventually. But it just keeps falling. And they want out. That’s what I think happened here.

I’ve written about Yanis Varoufakis a few times. I check him out whenever there’s a flare up in Greece. There’s one now, so I headed over to his blog and found that he’ll be running on the SYRIZA ticket. He seems a genuine guy, with some really whacked out ideas on centralizing the entire European banking system with a bunch of bonds he made up in his head.

If I remember correctly, he wants Greece to default on the debt, liquidate it, and stay in the Eurozone nonetheless. If this is what he really wants, he won’t be able to accomplish it in SYRIZA. SYRIZA wants an end to the bailout scheme, which is doing nothing but putting Greece into even more debt (it’s debt to GDP has not fallen contrary to popular perception) and at least that aspiration is a good one. But what SYRIZA wants instead is an end to austerity and a free ride to keep spending.

If Varoufakis actually wins a seat, which seems likely, he will likely start to butt heads with his pretty-boy party leader Tzipras, a far leftist who thinks prosperity is invented out of nothing by the good graces of politicians like himself.

End the bailout Varoufakis and Tzipras will agree on. What happens after that, and they’ll start fighting. Tzipras will want more spending, which if he pushes it, will end up pushing Greece out of the Euro by force because Europeans (by which I mean Germans) are not going to finance it anymore. This, Varoufakis doesn’t want. And if they do get pushed out, there will almost certainly be hyperinflation in its drachmas within weeks.

So let’s see what Yanis does. He writes:

My greatest fear, now that I have tossed my hat in the ring, is that I may turn into a politician. As an antidote to that virus I intend to write my resignation letter and keep it in my inside pocket, ready to submit it the moment I sense signs of losing the commitment to speak truth to power.

Keep that letter handy Yanis. You’re going to need it once you see that your fellow politicians are not going to want to cut their spending.

The global financial system is like a lake right before a limnic eruption. I just learned about this phenomenon from Scishow.

A limnic eruption is when a lake explodes. Carbon dioxide leaks into it for centuries from magma below, and if the lake is stagnant and the water doesn’t circulate much, any little thing can set it off. When it does, all the dissolved carbon dioxide below wells up to the surface and the whole lake blows up, together with a cloud of carbon dioxide that suffocates everything within a several mile long radius.

Anything can set off a chain reaction that will bring down the entire global sovereign bond market. I don’t know when it will happen, but the next thing in line as a candidate to light the fuse is, once again, Greece.

I just read a particularly horrendous article in The Guardian about this. The situation is like so. Two years ago or whatever it was, Greece agreed to a giant bailout in return for cutting its budget. Unemployment is above 25% in Greece and poverty is in the 40% range.

The point of cutting its budget is obviously to lower its debt, for the government to spend what it takes in only, and – a totally radical idea – run surpluses to actually pay some of it back, like normal people in debt do. Instead of Ponzi Scheming your way into “rolling over” the debt, meaning paying back old debt with new debt.

So here’s what the “Austerity” in Greece from “draconian” government budget cuts looks like since 2012.

Since “Austerity” began, the debt went up.

The problem now is that Greece is having trouble naming a president. There is one final round to do this on December 29, and if their politicians fail to name a head politician, a party called Syriza will likely come to power in snap elections (like the ones here in Israel on March 17). Syriza wants no more “Austerity”. Meaning, they want to spend more.

Well that’s nice, but more of what, exactly? Euros? You’re being cut off. Drachmas? Who the hell is going to trust that piece of paper when you can’t pay back a damn bond? Look for money, you ain’t got none. Comb the desert like they did in Spaceballs, and “We ain’t found S$*T.”

I will pick apart the worst parts of this guy Owen’s gross follies, but in a general sense, his problem is that throughout the whole piece of garbage, he equates prosperity with government spending. Because the government cut its budget, that’s why people are poor.

Prosperity is proportionate to economic freedom, not government spending. Greece has very little of the first, and a LOT of the second.

Real government austerity would be cutting the bureaucracy down to bare bones nothing. Let businesses start up with no papers, no permits, no nothing. Let people work with no documents, no restrictions, no rules except no slavery. Open up your borders to all imports, all exports, lower taxes to almost nothing except to keep courts and an army running. Default on all bonds and let the bondholders take the losses. Let money arise organically and stop printing it. That’s all you have to do. Greeks are not idiots. They know how to produce things. They have simply grown accustomed to government handouts and now that the pig trough has run dry, they want more but there is nothing left.

Here are some of the worst lines from the article:

What misery has been inflicted on Greece. One in four of its people are out of work; poverty has surged from 23% before the crash to 40.5%; and research has demonstrated how key services such as health have been hammered by cuts, even as demand has risen.

Owen doesn’t understand supply and demand and monopolies, while he probably opposes the latter in word, but not in deed. When a single entity is in charge of providing a service and others forbidden by government from competing, or if one single entity is heavily favored and subsidized by government over potential competitors, that is a monopoly. In a monopoly, supply and demand do not work because the price mechanism is broken. So the monopoly, like a health services monopoly, can cut services even when demand rises, and make the same amount of money because it can charge whatever it wants. There are no competitors. This is what happens in monopolies. The solution is to get rid of the monopoly, end government health services completely, and let anyone treat anyone however they choose.

This though, is the worst:

Syriza’s manifesto proposes that repayment of debt could come through economic growth, rather than from budget cuts. It wants a European new deal backed up by an investment bank; an all-out war against the tax avoidance endemic in Greek society; an emergency employment programme; a raised minimum wage; and the restoration of collective bargaining.

How in hell are you going to pay back 175% of your entire economy through “growth” while at the same time supporting a massive-sized government that got you bankrupt in the first place?! Even worse, if you’re complaining about 40% poverty, how is an “all-out war against tax avoidance” going to make anyone richer?! They’re in poverty as it is, and you want to end tax avoidance? Meaning that if these poor poverty-stricken people pay more taxes to YOU, Syriza, everyone will be richer?

An “emergency employment programme”. That sounds terrifying, especially when it comes just before “a raised minimum wage”. When 25% of the entire country is unemployed, you want to make it even harder for people to get a job?! Here’s my “emergency employment programme”. Zero taxes or regulations on starting a company. Zero restrictions or regulations on hiring people. That’s it. I have a better idea than increasing minimum wage. Make it a law that employers must keep hiring until unemployment reaches 0%, or else they go to jail. How about that?

Here’s just wacky psychobabble:

That’s why Greece desperately needs solidarity. Firstly, there’s a point of principle: to defend sovereignty and democracy from attack, whether from within or without. But a Syriza government could spur on other anti-austerity forces across the continent.

Can anyone extract any meaning from these sentences? Greece needs solidarity. OK. Sounds all nice and cheerleadery. “Defend sovereignty and democracy from attack from within or without” – do these words say ANYTHING? What do they mean? They mean nothing. It’s just meaningless pep talk from a sophist. “Anti-Austerity forces across the continent” – WHAT austerity? THIS?

Austerity is when spending goes down, not stays the same.

Is it THIS?

Isn’t debt supposed to go DOWN when you’re being “austere”? Isn’t that the DEFINITION of austerity?

So how could Greece be a limnic explosion? If Syriza is elected, they will try to increase government spending with money that does not exist, and get kicked out of the Euro for trying. Greek bonds will default, banks holding those bonds will need bailouts or crash, and the bonds of other weak Eurozone governments like Italy and Portugal will plummet, pushing yields up to the point where the Ponzi Scheme no longer works because there are no new suckers to buy the new bonds and roll over the debt.

From there, once a country the size of Italy goes down, that’s a LOT of bonds, and the whole global financial system could explode, suffocating all those who have not insulated themselves from the explosion.

Will this happen? Yes, eventually and soon. Will it necessarily happen this way? No. But we’ll see.

Government of Country A wants money to bribe citizens of A for votes.

Government A goes into debt by selling bonds, and gives money to people of A, and gets reelected.

Government A needs more money, so it sells more bonds, and gives it to people of A.

Government A sells so many bonds that debt surpasses GDP of A. People get worried that A will not pay bonds. Interest rates rise.

ECB buys hundreds of billions in bonds of A to “stabilize the system”, and gives A the money it printed to buy them, in exchange for going even deeper into debt.

A defaults, ECB stops giving them Euros.

A leaves the Euro and prints its own currency.

Currency A plummets in value because nobody else wants it. People of A have nothing to exchange for goods and services. They starve and riot.

Debt is encouraged in a fiat system because in the back of their minds, investors always know the central bank will guarantee the bonds, enabling countries to go so deep into debt that they will never be able to pay it back. How would it work under a gold standard?

Government of B wants to bribe its citizens for votes.

Government A goes into debt by selling bonds for gold, gives gold to people of A, and gets reelected.

Government A needs more gold, so it sells more bonds. But they can’t sell as much since investors are trying to conserve gold rather than keep lending it to A. Interest rates rise.

Investors in A’s bonds are literally running out of gold. They stop buying bonds in order to conserve gold for other purposes.

ECB does not buy any bonds either since ECB does not exist. Gold is money and it is spread around, given in exchange for goods and services.

A’s debt is large, but manageable, because nobody allowed them to go too deep into debt in an attempt to conserve their gold reserves.

A cuts its budget, stops borrowing gold, and begins to pay back its debt in gold by exchanging goods and services for gold. Life is harder, but the budget is eventually balanced and the debt is repaid.

In the next election, people of A elect fiscal conservatives who understand that it is a bad idea to go too deep into debt.

Aside from the fact that the mantra is repeated by virtually every media outlet, mainstream and otherwise, why should any Eurozone country defaulting have anything to do with that country leaving the Euro? Except for Yanis Varoufakis, who is virtually the only Keynesian econometrician who seems to have a workable solution for Europe, everyone else just assumes that default equals exit. Why should this be?

Take the United States for example. The US is a dollar zone. All fifty states use the dollar, and California is about to go bankrupt. Is anyone seriously discussing California leaving the dollar zone if it defaults on its debt? No. Miami, where I come from, declared bankruptcy when I was a kid. Did anything happen to my family? No, because we weren’t stupid enough to buy the municipal bonds of a bankrupt municipality. And by the way, Miami did not exit Florida after it went bankrupt. As it should happen in a bankruptcy, those who own the debt lose the money. That’s it.

So why are we even discussing Greece “leaving the Euro”? Why should they? How does that help anything? Who decides if they are going to be kicked out? Who is in charge of the Eurozone who makes these decisions? Why should it even be an option? What is going on here, has anyone asked these questions?

If Greece did “exit,” it wouldn’t be Greece leaving of their own accord. What would happen is that the European Central Bank would stop giving Greece euros to fill their ATMs, and the country would literally run out of currency and they would have to start printing their own. So the answer is whoever is in charge of the ECB makes these decisions.

Who is in charge of the ECB? Mario Draghi, an Italian? I doubt he’s the one who’s going to make the final decision to stop giving currency to a Eurozone member.

Whoever has his hands on the switch is probably in Germany. The implication is that the Germans literally control Europe. They decide who’s in, who’s out, who starves, who lives, who dies. Germany conquered Europe. Again. Without anyone noticing. It’s August 31, 1939, but instead of Poland, the Krauts are about to invade Greece.

It’s interesting. We always thought World War III would be started with a nuclear bomb. It looks more and more likely that it will be started with a printing press.

The New York Times is reporting today (June 6) that Greece is running out of money to pay its immediate obligations. This is mostly because they’re not getting enough bailout money because the bailer outers don’t know if Greece’s next government will agree to the terms of the bailout, and Greece doesn’t have a government yet because the Greeks couldn’t decide whether or not they want to agree to those terms. So another election is scheduled for the 17th, elections cost millions of Euros which the Greeks don’t have, and in the meantime they have no money left.

The terms, by the way, are that Greece must commit suicide if they are to be able to collect on their bailout.

The budget gap is widening as the so-called troika of lenders — the International Monetary Fund, the European Central Bank and the European Commission — withholds 1 billion euros in bailout money earmarked for government financing while it waits to see whether new leaders elected June 17 will honor Greece’s commitments.

Even if the troika delivers that money, Greece will struggle to cover its obligations. It underscored a harsh reality that is playing out in other troubled euro zone economies. Prolonged austerity is making it harder, not easier, for governments like Greece to become self-reliant again.

What the New York Times isn’t telling you is that the ECB is making a nice profit off the so-called Greek austerity, which is only inflating Greek debt all the more. Yanis Varoufakis calls it “ponzi austerity”.

Meanwhile, Spain is complaining that nobody wants to lend Spain money anymore. They warn that if that happens and nobody lends Spain money anymore, they won’t be able to pay back the money they owe to other people who lent them money in the past. So they need new money to pay back previous lenders.

The Ponzi scheme is about to end! Quick! Somebody print some Euros for the love of the Eurozone!

Tomorrow there’ll be something about Italy. Just end this thing already and put Europe out of her misery.